Feb 4, 2006

By Bonddad,

bonddad@prodigy.net

I have written a great deal about the US economy's over-reliance on debt at the Federal and household level. This over-reliance is one of the prime reasons why I have been and still am concerned about the health of the US economy. Instead of actually owning our growth, we have yet to actually pay for it. Most importantly, as the analysis below highlights, if the bill comes due suddenly we could be in for a very rude awakening.

The following analysis is from MacroMaven's Stephanie Pomboy. I will add further comment on her analysis.

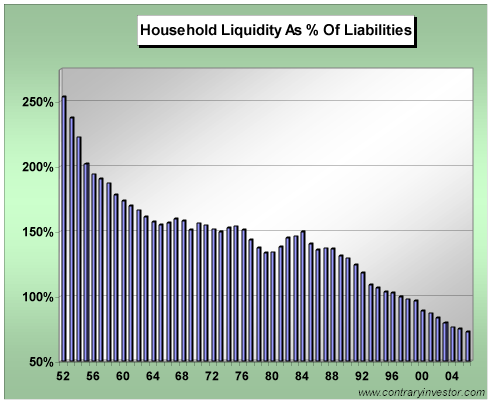

First, we are going to measure US household's cash holdings as they relate to debt. The purpose of this analysis is to determine US household's ability to actually pay off their debt. Here is how they measure cash:

In the following charts we are looking at household liquidity or cash, as we term it. They are synonymous in terms of calculation. For this number we are adding together all household bank deposits, CD's, money funds, checking accounts, savings, and other bank-like products together with all household bond holdings inclusive of Treasuries, corporates, muni's, agencies, etc. Long time readers know we try to apply the most broad measure of liquidity to the household picture when examining these trends. Implicitly we are assuming bond investments could be converted to cash with ease. Not included is real estate, stock holdings and private business equity ownership, but that's about it. In other words, we are trying to give households the most broad benefit of the doubt when reviewing their liquidity circumstances. Here we go.

What we are looking for is quick cash -- cash that households can access quickly in case of financial emergency. Real estate can take a long time to sell, and taking out a home equity loan can not only take time, but is simply swapping one form of debt for another. Equity in a company can't be sold quickly and would have a large number of stipulations attached to it if the owner wanted to use it as loan collateral. Stocks are usually held in a retirement account, which means there is a substantial penalty for early withdrawal.

The chart above is very telling. Simply put, if all the bills came due, households would not be able to pay them all off. Here's another way to look at the same idea -- total cash minus total liabilities. As the author notes:

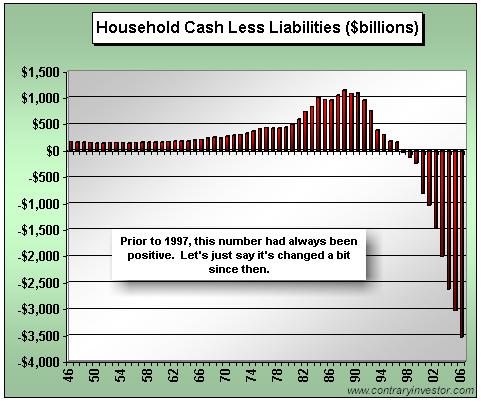

A bit more dramatic is what lies below. It's the same concept as above just expressed in nominal dollar terms. This time we're looking back six decades. As we detail in the chart, never prior to 1997 was household liquidity less than total household liabilities. But as you know, also since that time the household savings rate has plunged and household liabilities have mushroomed. All part of greater credit cycle dynamics playing out before our eyes.

Short version: there just isn't enough cash to pay the bills if they all come due. Now you should understand why the credit industry was so pushy about the changes to national bankruptcy law a few years back. The industry wanted to make sure they got paid in the event of default.

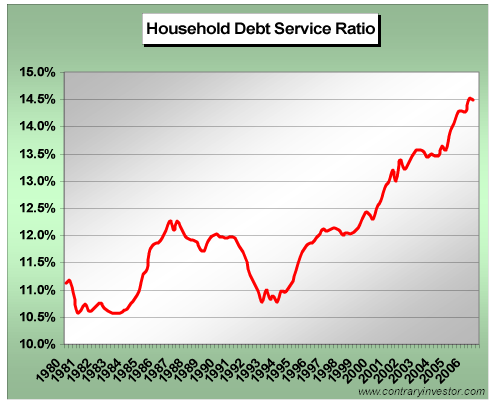

And households debt payment levels are at record levels:

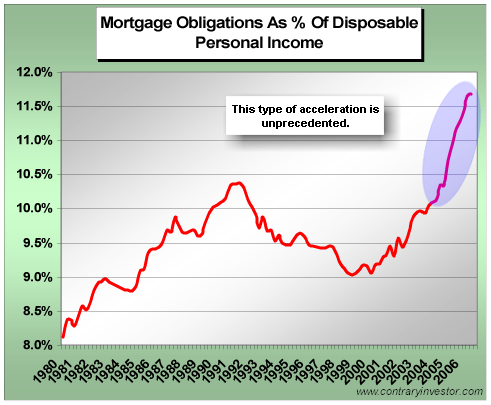

One of the main reasons for the increase is mortgage debt, which has ballooned over the last 6 years.

The authoer makes a very interesting observation which is worth noting:

As we've mentioned many a time, what we are seeing in these charts is an intergenerational change in attitudes toward leverage. It's a change in comfort with leverage.

This is certainly one way to look at the whole picture -- that people are much more comfortable with going into debt, are more savvy about managing it and are simply more comfortable with all of debts ramifications. Or -- maybe the credit industry as a whole has used aggressive and possibly deceptive marketing techniques to sell debt without completely explaining the ramifications of debt to customers. The truth is probably in the middle of those two statements.

However:

But we will be the first to admit, in nominal dollar terms, the magnitude of the change you see above is more than a bit striking. Much more, as a matter of fact.

This really hits the nail on the head. While using debt can be financially benficial in certain situations, the extent of the change over the last 10 years is striking.

For economic analysis and commentary, go to the Bonddad Blog

No comments:

Post a Comment